07/03/2023

Over a year has now passed since the start of the Russo-Ukrainian war, the introduction of sanctions, and the reciprocal closure of western, Russian, and Belorussian airspace to select foreign registered aircraft. This naturally posed a huge challenge to European, Asian, and Russian operators as they worked hard to recover from the Coronavirus pandemic.

Finnair elected to use the polar route to reconnect services to Japan, and the southern route to Southeast Asia and China. Flight data from IBA Insight reveals that Finnair operates the same number of flights into Singapore and Tokyo today as they did in 2019, but with increased flight durations on each route of 13% and 31% respectively. The airline’s utilisation of the A350 (with its 300 min ETOPS certification) has helped the carrier adapt flexibly. By contrast, operators such as Scandinavian Airlines have elected to remove Japan from their network altogether and have resumed only 7% of Chinese flights to-date.

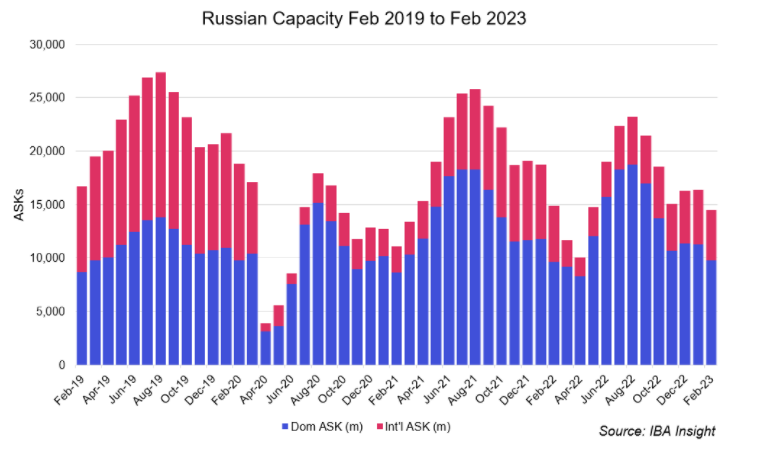

Russian operators were, in fact, leading the way in post-pandemic recovery with domestic ASKs already 10% above the 2019 peak by August 2020 and 32% by August 2021. Most notably, domestic ASKs sat at 36% above peak 2019 levels in August 2022, following 4 months of sanctions! Whilst we anticipated domestic growth as a result of a big fall in international capacity, I would have expected the sanctions to have dented passenger traffic to a greater extent.

Whilst IBA Insight reveals that flights have reduced by around 11% since 2021, we have also observed flexibility in the utilisation of the Russian fleet. Usage of the A319, 737-700 and 737 classics has reduced in favour of increased deployment of the A321. Furthermore, we have witnessed a 20% increase in the usage of widebody aircraft on domestic routes, placing more reliance on the A330 and 777-300ER, the latter of which has seen a 111% increase in flights. Russian operators halted passenger A350 operations in 2021, and these aircraft were largely grounded at the onset of sanctions.

International Capacity was down by 79% in 2020, recovering to 44% below 2019 levels in 2021. This reduced again to 67% below 2019 levels following sanctions. The number of countries visited by Russian operators had dropped from around 80 to less than 30 by the summer of 2022.

The most popular summer destinations for Russian travellers proved to be Turkey (37% of capacity), followed by Tajikistan, Uzbekistan, UAE and Kyrgyzstan (each with around 10% capacity).

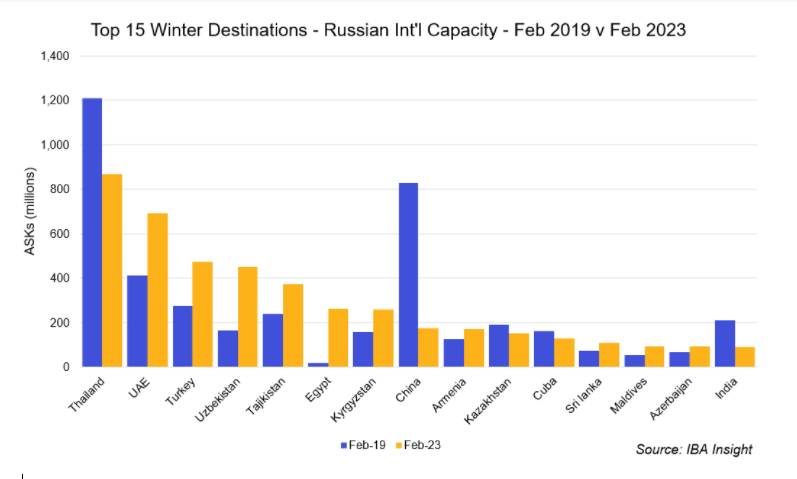

Winter destinations tell a different story. As of February 2023, Thailand tops the list with 19% of the capacity, followed by UAE with 15% and Turkey coming in third with just 10% (just 29% of summer 2022 capacity). Worthy mentions also include Egypt, Cuba, Sri Lanka, the Maldives, and India. These collectively account for 15% of winter capacity but <5% of summer 2022 capacity.

Egypt is proving a noteworthy winner, with a 1300% increase in traffic to the country from Russia. This has been buoyed by limited options, and the 2021 lifting of the ban on direct flights to Egyptian resort cities following the crash of Metrojet flight 9268. Locations such as the UAE, Turkey, The Maldives and Sri Lanka are up 50-75% on 2019, whilst Russia’s largest winter sun location, Thailand, still has some ground to catch up.

Myself and the team will continue to monitor and report on the evolving situation for Russian carriers and the impact on lessors and the wider aviation finance community.

The IBA team share regular insights on all aspects of commercial aviation, from airline capacity and travel trends to aircraft values and ESG strategy. Sign up today to get the latest intelligence from the IBA Weekly newsletter delivered straight to your inbox.

Share this article

Author

Related content

IBA House, 7 The Crescent,

Leatherhead, Surrey KT22 8DY